I mentioned in a post last week that I think this may be a bad time to buy a house. I thought I would elaborate on this just a little bit. No, this isn’t a financial blog and I’m not a financial expert. I have no financial training (other than what my dad has been teaching me over the years and the regular reading I do on the subject) and no one should make any decisions based on what I say here, blah, blah, blah.

However, knowing that a lot of people (read: women – sorry to generalize) don’t necessarily follow financial news, I thought it might be prudent of me to mention this and people can do whatever they want with it.

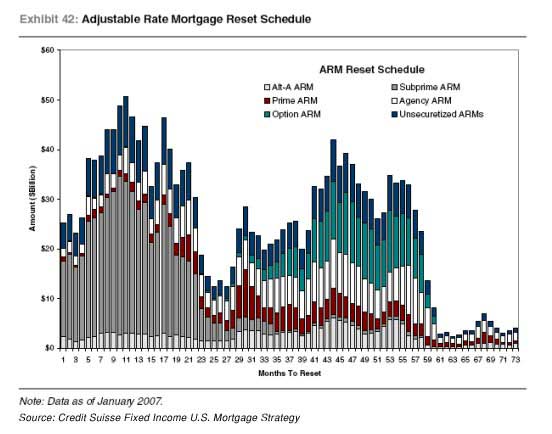

While this chart does not summarize the entire situation, I think it goes a long way to getting the conversation started. This little beauty was put together by Credit Suisse, probably a pretty recognizable name to most readers here.

Ok, so what does it mean? ARMs are Adjustable Rate Mortgages. Gazillions of homes have been purchased using ARMs over recent years. They start out with low teaser rates (1% interest for first year or two, etc. – I’m sure you’ve seen the ads all over tv in recent years). However, then they adjust – UP. Sometimes a lot. Sometimes a lot many times. So people who start out being able to make their payments find that in a few years they can’t. When that happens, they lose their house. Think foreclosures, bankruptcy, etc.

Now there isn’t necessarily anything wrong with ARMs when they are used in a proper situation (and there aren’t many of them that really are appropriate). What is wrong is that many of the ARMs that have been taken out are of the subprime variety. These are people who have bad credit histories and would never qualify for a traditional 30 year mortgage with 20% or even 5% or 10% down. There has also been a lot of mortgage fraud with no documentation loans in order to get people into these loans. So some guy who works as a janitor making $14,000 a year somehow qualifies to buy a $350,000 house in California. The rampant fraud is a whole nother story.

(I realize I’m glossing over big areas here, but I’m trying to just give an overview so people will investigate on their own.)

Ok, now look at the graphic. This graphic starts in January 2007. It shows the number of ARMs that will reset for the next 73 months. That is between now and 2013 if my math is correct. So far we are four months into this. Notice that although some ARMs have started resetting, the vast majority of them are yet to come. In fact, the first big uptick starts next month (June).

If you follow the news at all, I’m sure you have already heard about the slowdown in the area of real estate. Perhaps you’ve noticed that there are a lot of houses for sale right now where you live. You’ve heard about foreclosures. The National Association of Realtors (NAR) announced that sales of existing homes dropped 11.3% in March compared to the previous March. This is the biggest drop in 18 YEARS. March foreclosures increased 43% compared to last year to almost 150,000.

Now look at the graph again. We are FOUR MONTHS into this. The graph covers 73 MONTHS. And already there are a lot of people in a world of hurt.

Another aspect to consider is that a lot of people have been using their homes as ATMs over the past ten years. As home prices have continued to rise, people have taken their (perceived) equity out of their houses time and time again. Many people live in houses in which they have NO equity because they have taken it all out.

Yet another aspect to consider is the widespread speculation throughout the country. A lot of the run-up in housing prices is due to speculators. Speculators are trying to dump the homes they intended to flip for a quick buck.

But what does this have to do with me buying a house, Sallie? I’m glad you asked!

Let’s say John and Jane live on a street with twenty houses. There are a hundred houses in their development. They paid $200,000 for their house and they were able to get a conventional mortgage by putting down 20%. So in theory they had $40,000 in equity in their house when they moved in. For the sake of argument, let’s say that the houses on their street are all pretty similar. They might vary in price by no more than $10,000 – $15,000.

Unbeknownst to John and Jane, a few of their neighbors have been living off their equity in recent years. John and Jane could never figure out how their neighbors could afford the new SUVs and multiple trips each year, but that was how they did it. So their neighbors technically don’t have any equity in their houses. Another neighbor had terrible medical bills and made the same choice – to use the equity. A couple of their neighbors are new. They purchased their homes with subprime ARMs. They put 0% down so they don’t own anything in their house either.

Well, as life goes, things start to happen on their street.

- One couple retires and decides to sell. Since they are anxious to relocate closer to family and aren’t desperate for money, they sell their house as soon as they get a reasonable offer – one that is a little lower than what John and Jane would have expected.

- One of their neighbors with an ARM falls behind on the payments when the interest rates adjust, the bank forecloses, and then lists the house. Since the bank wants to unload it, they lower the price a bit and it sells.

- Another neighbor follows the financial world and is concerned about what he perceives is happening in the housing market. He decides now is the time to sell before prices really start dropping. Since he has a lot of equity in his house, he decides to unload it and is even willing to take a bit of a price cut in order to be sure he gets his money out.

- Another neighbor with an ARM doesn’t make it and loses the house. It gets auctioned off on the courthouse steps to the highest bidder – of course, at a bit of a lower price.

- Another house is purchased by a speculator from another state and he decides to cut his losses and unloads his house just to stop the financial bleeding.

Even though John and Jane haven’t done anything, based on the comps for their neighborhood, their house value is declining.

Now suppose John and Jane want to relocate for a new job. They need to sell their house and you look at it. They want $240,000 for it because of course real estate always goes up and they certainly should have some appreciation for all the months they’ve been making mortgage payments! Would you pay $240,000 for a house when the houses around them have been going in the $160,000 – $190,000 range? Of course not!

But suppose you really love the house and you are able to get John and Jane to come down to $200,000. Is it still a good buy? Maybe if you plan on living there for a long time and can afford to have property values continue to drop. But who knows where the bottom will be? How many more houses on that street and in that development are going to be sold at lower prices in the years ahead as the ARMs continue to reset? Do you want to pay $200,000 for a house and then find out in three years it is only worth $125,000?

If you put 20% down on that house, that means in just three years time you will be underwater. You will owe approximately $160,000 on a loan for a house that is only worth $125,000 on the current market. Do you look forward to making payments on $35,000 worth of house that really doesn’t exist? What happens if you need to relocate and need to sell? Will you be able to absorb a $35,000 loss as well as pay all the realtor fees out of your own pocket?

But you say, Sallie, prices can’t possibly drop that much! I say – look at that graph again. There are still 69 MONTHS ahead with a lot of people in houses they will never be able to hang onto. Who is going to buy them? Who is going to pay full price for them? Much of the recent economy has been based on this unrealistic run up in housing. The homebuilders are announcing all the time how their sales are off 30%, 40%, or 50% over the previous year. Think of all the people who aren’t going to be making much of a living as this thing unfolds – think almost everyone associated with home building. Think how that trickles into the rest of the economy.

So my thought is this… If you can afford to buy a house and see it depreciate in value over the next several years, then maybe it is ok for you to buy. If the desire to have a house that you will live in long term outweighs a $10,000, $15,000 or $20,000+ drop in value, then maybe you are ok. (If you live in some parts of the country, the drop may be measured in the $100,000s, not $10,000s.)

And by long-term we’re talking fifteen, twenty, thirty years here, folks, not flipping in five years.

So that’s why I think this may be a bad time to buy a house. I could be completely wrong. And if I am, I will admit it. If I’m wrong, I don’t figure David and I have much to lose. We stay in our house, keep making our payments, and our house continues to appreciate in value. But if I’m right and we bought an overpriced house, it really could be a financial disaster.

So that’s the quick version. I’m sure I’ve probably left a lot out, but I wanted to keep this brief to just raise the question in people’s minds.

Oh, speaking of people’s minds. Some people might say that this whole housing bubble thing is just happening because people like me are writing about it. If people would just stop writing about it, it wouldn’t happen.

Um, no. (And the explanation of that answer is another post.)

But even if you are right, remember that when it comes to something like this perception is reality. If people perceive there is a problem, there will be a problem because people will act accordingly. So you can argue there is no bubble, but if enough people believe there is a bubble, there will be consequences. Almost two years ago when I wrote about this the first time (and then a second time), almost nobody even knew the term housing bubble. I venture most people have heard of it now. In fact, I would guess most people know someone in trouble with their house and it is just getting started.

So, do your homework and pray, pray, pray. Make sure you know what you are getting into and be sure that you have the confidence God is leading you to make the right decisions.

Edited to add: Here is a link that will take you to a great post with details like I am talking about. These details are all from the mainstream media and are actually worse than the scenarios I discussed above. Warning: Comments after post have pr*fanity.